Navigating Corporate Governance Reporting in ASX Listed Companies

- contactadvacta

- Nov 3, 2023

- 3 min read

Updated: Nov 3, 2023

Corporate Governance Obligations under ASX Listing Rules and Corporate Governance Principles and Recommendations (CGPR) 2019

Corporate Governance Statement

Under ASX Listing Rules, listed companies are required to prepare a corporate governance statement. This statement must include information on the company's compliance with the Corporate Governance Principles and Recommendations (CGPR) 2019 during the reporting period, and explanations for any departures therefrom. Corporate governance statement must either form part of the annual report or separately disclosed on the company website. CGPR 2019 contains 35 general recommendations and 3 additional recommendations.

Appendix 4G

Listed companies are also required to prepare and lodge an Appendix 4G, which is a way for companies to confirm whether they have complied with the Corporate Governance Principles and Recommendations (CGPR) 2019 recommendations. Appendix 4G also acts as a guide for users to locate the governance disclosures made by listed companies.

Appendix 4G must be lodged with ASX at the same time as the company gives ASX the annual report. In any case, it must be lodged no later than four months after the end of the company's financial year.

Overlap Between CGPR 2019 and Listing Rules

While compliance with CGPR 2019 is not mandatory, and operates on a “If not, why not” basis, non-compliance of certain recommendations could lead to a breach of listing rules.

For instance, CGPR 2019 4.1 recommends that listed companies should have an audit committee, and specifies composition and disclosure requirements for the same. Listing Rule 12.7 mandates listed companies of a certain size to have an audit committee and adhere to CGPR guidelines. Such companies are required to comply with CGPR 2019 4.1 in full or it would result in a breach of Listing Rule 12.7.

Appendix 4G and Corporate Governance Statement of 100 ASX Listed Companies

We examined the corporate governance disclosure practices of Top 100 ASX listed companies by market capitalisation in our 2023 Governance Impressions Report.

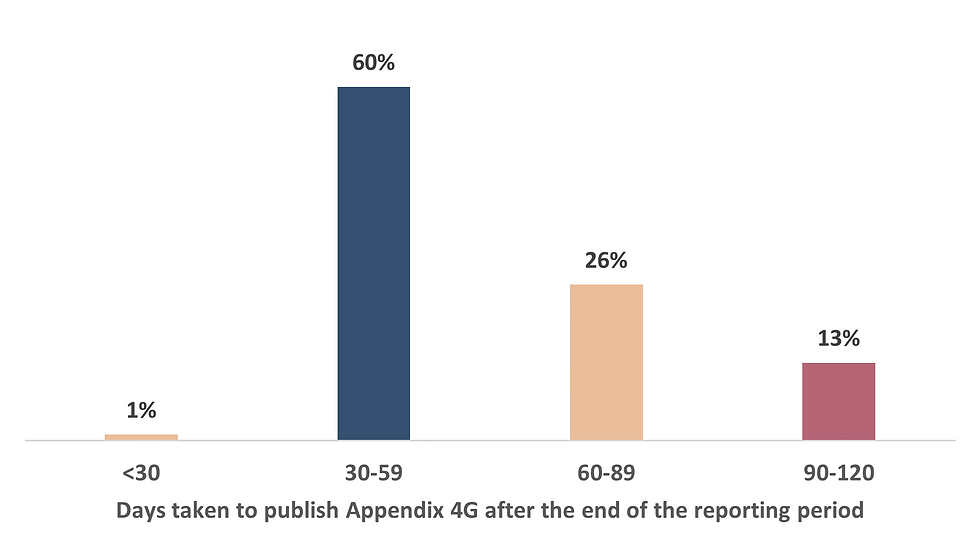

We found that 61% of the companies published Appendix 4G not later than 60 days from the end of their reporting period. 13% of companies took 90 or more days.

Least Followed CGPR Recommendations

Other CGPR Recommendations Not Followed

CGPR 1.3: Written agreement with director and senior executive

CGPR 3.1: Disclosure of company values

CGPR 3.3: Whistleblower policy

CGPR 3.4: Anti-bribery and corruption policy

CGPR 4.1: Audit committee

CGPR 4.2: CEO and CFO Declaration

CGPR 7.1: Risk committee

CGPR 7.4: Environmental and social risks

CGPR 8.1: Remuneration committee

Disclosure Practices

Corporate Governance Statement (CGS)

Appendix 4G

While disclosures in corporate governance statement are expected to present a wide variance as governance practices depend on the size and requirements of the companies, disclosures in Appendix 4G ought to be fairly uniform. However, we still observed diverse practices in Appendix 4G.

Take gender diversity for example. As per CGPR 1.5, companies should set and disclose measurable objectives for achieving gender diversity in its board of directors, senior executives, and overall workforce. They should also disclose the extent to which the objectives have been achieved. For a company in the S&P / ASX 300 Index at the commencement of the reporting period, not less than 30% of the board of directors should be composed of each gender within a specified period.

Gender Diversity Disclosure in Appendix 4G

The purpose of a corporate governance statement is to ensure that reasonable information is available to the investors about the company’s corporate governance practices. Companies are expected to provide a detailed and transparent report, which will help shareholders to understand the company's governance practices and make informed voting and investment decisions.

If a company has chosen not to adopt the CGPR principles in full or reports non-compliance during the reporting period, it is required to explain the reasons for the same. However, in many instances, we found that the explanation was perfunctory without yielding any useful information. Homogeneity in disclosures through the establishment of quantitative disclosure criteria would be helpful in making comparisons and ascertaining to the extent to which CGPR recommendations have been implemented.